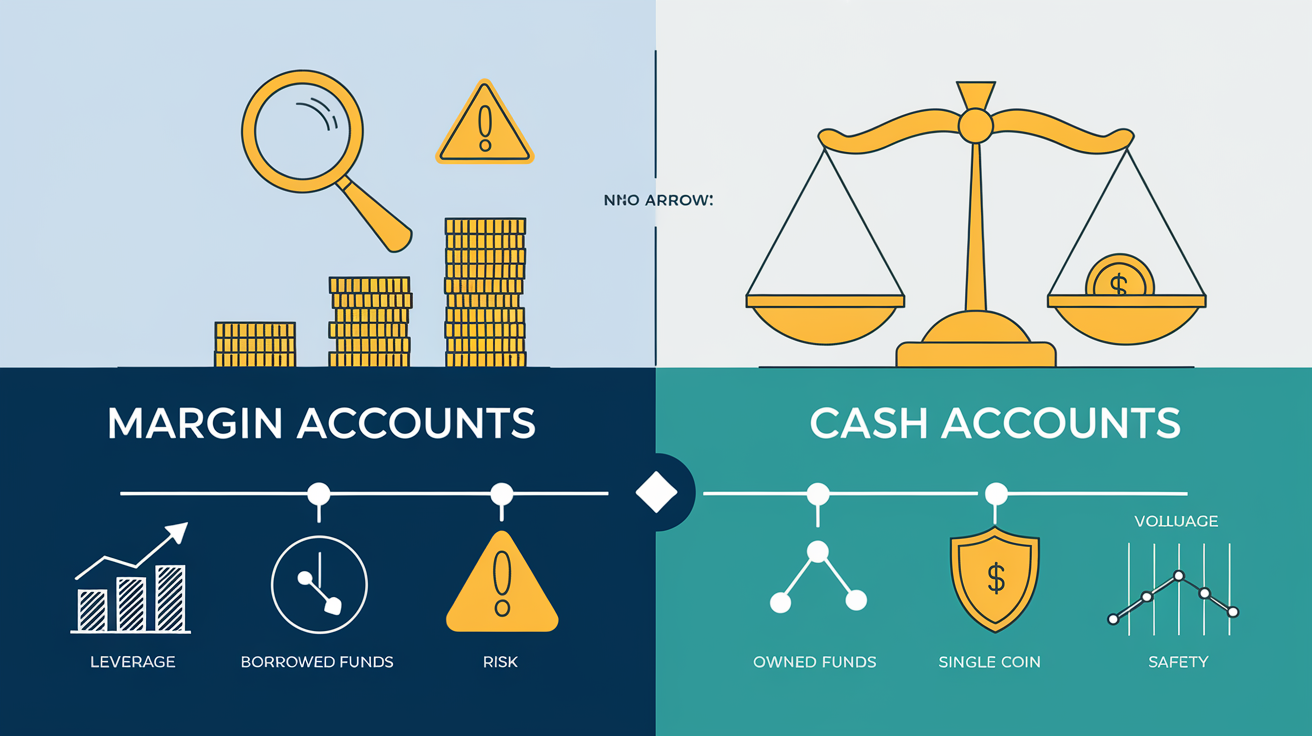

I'd say the main difference between a margin account and a cash account comes down to borrowing power and risk. With a cash account, I only trade what I can afford, paying upfront for everything. It's safer but limits my trading options. A margin account lets me borrow money from my broker, enhancing my buying power for things like short selling or options. Sounds great, but it's riskier—I could lose more than I put in, and market dips might trigger a margin call. If I'm careful, though, it can be a powerful tool. There's more to investigate if you stick around.

Key Takeaways

- Cash accounts require full payment for securities; margin accounts allow borrowing to increase buying power.

- Margin accounts support advanced strategies like short selling and options; cash accounts limit trading to available funds.

- Margin accounts have higher risks, including potential margin calls and forced liquidation; cash accounts restrict losses to deposited funds.

- Margin accounts incur interest costs and higher fees; cash accounts avoid borrowing expenses and associated risks.

- Min. equity requirement for margin accounts is 25%; cash accounts have no borrowing or maintenance requirements.

Cash Account Basics

In a cash account, I pay the full amount upfront when buying securities, which means I can't borrow or use financing. This is the most straightforward way for investors like me to trade without taking on debt.

When I make a purchase, the transaction settles quickly, usually by the next business day, so my money isn't tied up for long. Cash accounts keep things simple—I can only trade with the money I've deposited, which prevents me from overspending or getting into risky situations.

While I mightn't have access to advanced strategies like short selling or unfunded options, I also avoid the stress of owing money. Plus, any uninvested cash in my account can earn a bit of interest through a money market fund, which is a nice perk while I'm waiting for the right investment opportunity.

Cash accounts are perfect for investors who prefer a no-fuss, low-risk approach to trading. They're like paying with cash instead of a credit card—what you have is what you can spend, and there's no bill to worry about later.

Margin Account Basics

While a cash account keeps trading simple, a margin account opens up more opportunities by letting me borrow funds from my broker to buy securities. Margin accounts let me amplify my buying power, but they come with added responsibilities, like maintaining enough equity to meet the maintenance margin requirement. Typically, I need to keep at least 25% of the total market value of my securities as equity. If my account falls below this, I'll face a margin call, forcing me to deposit more cash or sell assets.

Margin accounts also allow for advanced strategies like short selling or purchasing options, which I can't do in a cash account. However, I'll pay interest on the borrowed funds, so I need to factor that into my returns. It's a trade-off: more potential for gains, but also more risk.

Here's a quick breakdown of key differences:

| Feature | Margin Account |

|---|---|

| Borrowing Power | Lets me borrow funds |

| Minimum Equity | Must meet maintenance margin requirement |

| Advanced Strategies | Short selling, options trading |

| Interest Charges | Pay interest on borrowed funds |

| Risk of Margin Calls | Account equity must stay above threshold |

Leverage in Margin Accounts

Using control in a margin account lets me manage a larger position than my available cash would allow, as it enables me to borrow funds from my broker, typically up to half the purchase price of securities. This control can significantly improve my investment returns if the trade goes my way.

For example, if a stock I buy on margin increases by 10%, my gains are magnified because I've invested more money than I actually have. However, the flip side is that control can also amplify losses. A 10% drop might wipe out more than my initial investment, especially if I'm not careful.

Margin accounts require me to maintain a minimum equity level, usually at least 25%, to avoid a margin call. Falling below that threshold could force me to sell securities to cover the borrowed amount. Plus, I'll pay interest on the funds I borrow, which can eat into my profits.

While control can be a powerful tool, it's not without risks. I've learned to approach it cautiously, managing my exposure to avoid unnecessary pitfalls. Using margin wisely can enhance returns, but missteps can be costly.

Settlement Period Differences

Although settlement periods apply to both cash and margin accounts, the way they impact trading differs significantly.

In my cash account, I've noticed that every trade I make requires me to have enough cash available upfront, and I can't use the proceeds from selling securities until the settlement period ends, which is usually T+1. This means my money is tied up for a day, limiting my ability to jump on new investment opportunities quickly.

It's frustrating when I see a hot stock but can't act because I'm waiting for cash to settle.

On the other hand, my margin account lets me trade without worrying about the settlement period right away. I can use borrowed funds to buy more securities even if the cash from a previous sale hasn't settled yet.

This flexibility makes margin accounts work better for active trading, giving me more liquidity and the ability to capitalize on market moves instantly.

However, I'm aware that using borrowed money comes with its own set of rules, so I've to stay disciplined.

Understanding these differences helps me decide which type of investment accounts suits my trading style best. For instance, the level of risk associated with each account type can greatly influence my overall strategy. When comparing the performance and volatility of market indices like the Dow Jones versus S&P 500, it’s crucial to evaluate how each fits into my portfolio. By assessing my risk tolerance alongside these benchmarks, I can make more informed decisions about where to allocate my funds effectively.

Risk Exposure Comparison

When using a margin account, I'm taking on higher borrowing risk because I'm borrowing funds, meaning I could lose more than I initially invested, unlike with a cash account.

The pressure of margin calls is real—if my equity drops too low, I might've to add funds quickly or face the threat of forced asset liquidation, which isn't a concern in cash accounts.

While the borrowing might seem exciting, it's a double-edged sword that can cut deep if the market turns against me.

Leverage Risk Levels

Margin accounts expose me to higher borrowing risk since I can borrow funds to amplify my positions, which increases potential returns but also magnifies potential losses beyond my initial investment.

The amplification means I can control larger positions than my cash balance allows, but if the market moves against me, the losses can quickly pile up, even exceeding what I've put in.

This potential for increased losses is a double-edged sword—while I might see bigger gains during favorable conditions, a bad trade can wipe out more than just my original investment.

Additionally, the margin call risk looms large; if my equity dips below the maintenance threshold, I'll either need to deposit more funds or face forced liquidation of my assets.

In contrast, cash accounts don't let me borrow, so my risk is limited to the money I've deposited.

While borrowing can be tempting for its upside, the heightened exposure to loss makes it essential to weigh the risks carefully.

Margin Call Pressure

If my equity drops below the maintenance requirement in a margin account, I'll face a margin call, forcing me to either deposit more funds or sell assets to meet the broker's demands. This is one of the biggest pressures of margin accounts—sudden market downturns can quickly deplete my equity, leaving me scrambling to cover the shortfall.

It's like walking a tightrope; even a small dip in value can trigger a margin call, adding stress and uncertainty to my investments. Unlike cash accounts, where I'm only risking the money I've actually put in, margin accounts amplify the stakes because I'm borrowing to invest.

If I don't act fast, the broker can liquidate my assets to recover their funds, often at the worst possible time. Cash accounts, on the other hand, are simpler and safer—no borrowing means no margin calls.

While margin accounts offer the potential for bigger gains, they also bring the constant risk of these pressure-packed moments, making them a double-edged sword I need to handle carefully.

Asset Liquidation Threats

Though I often weigh the potential rewards of margin accounts, I can't ignore the looming threat of asset liquidation. When using borrowed funds, I'm constantly monitored to guarantee my account's equity stays above the broker's maintenance requirement, usually around 25%.

If my investments drop, I face margin calls, forcing me to either add more cash or liquidate assets to cover the shortfall. The pressure's real—market downturns can trigger forced liquidation of my holdings at prices I'd never choose.

Unlike a cash account, where my losses are capped at what I've deposited, margin accounts can wipe me out completely, especially if I'm over-leveraged. I've seen it happen: an investor caught off guard, scrambling to meet a margin call, only to sell at rock-bottom prices.

Cash accounts, on the other hand, keep me safe from this chaos. Without borrowed funds, there's no risk of forced liquidation, even when markets go sideways.

Sure, margin trading can amplify gains, but it's a double-edged sword. If I'm not careful, I could end up selling my investments at the worst possible time, just to settle my debts.

Trading Options Availability

When trading options, the type of account you've chosen significantly impacts what strategies you can employ.

With cash accounts, my options trading is restricted because I need to have enough cash upfront to cover the entire premium of the option I'm buying. This means I can't borrow funds, so my strategies are limited to buying calls or puts, selling covered calls, or using other fully funded, low-risk plays.

It's like being handed a toolbox with only a hammer and a screwdriver—it works for basic jobs, but I'm missing the tools for more advanced projects.

On the other hand, margin accounts give me much more flexibility in trading options. I can engage in uncovered (naked) options, spreads, and other complex strategies because the account allows me to use margin to cover premiums.

It's like upgrading to a fully stocked workshop. However, this comes with added risk, so I need to be cautious with borrowing. Some brokerages also limit options trading levels in cash accounts, so I often feel the pinch of restrictions compared to the freedom margin accounts offer.

Choosing the right account type really shapes my options game.

Margin Calls Explained

A margin call happens when the equity in my account drops below the broker's maintenance requirement, usually around 25% of my investment.

If I don't add funds or securities quickly, the broker can sell my assets to cover the shortfall, which can lead to unexpected losses.

To avoid this, I keep a close eye on my account and guarantee I've got enough equity to handle market ups and downs.

Definition and Basics

Margin calls are a key aspect of managing a margin account, and understanding them is essential. Unlike cash accounts, where you only trade with the money you have, a margin account lets you borrow funds from your broker to invest. This borrowing potential can amplify gains, but it also increases risk.

When the equity in your margin account drops below the broker's maintenance requirement—usually around 25% of the account's total value—you'll face a margin call. This means you must either deposit more cash or sell securities to bring your equity back to the required level. If you don't act, the broker can liquidate your assets without warning, potentially at a loss.

Margin calls are a reality of using borrowed money, and they can force you to sell investments during market downturns, making losses worse. While cash accounts avoid this entirely, margin accounts require active management and a clear understanding of the risks.

I've learned that staying informed and monitoring my account regularly is the best way to avoid surprises. It's not glamorous, but it's necessary if you're playing with borrowed potential.

Triggering Conditions

Although margin accounts offer greater investment flexibility, they also come with the risk of triggering a margin call if equity drops below the broker's maintenance requirement, typically around 25% of the account's total value. This maintenance requirement acts as a safety net for the broker, ensuring I don't overextend my borrowed funds.

But if the value of my securities declines and my equity falls below this threshold, the broker will issue a margin call. This essentially means I need to either deposit more cash or sell off some assets to bring my account back in line.

Market downturns are the usual culprits behind these calls. If I'm holding stocks that plummet, my equity shrinks, and suddenly, I'm under the maintenance requirement. It's like being asked to top up when you're already low on gas.

To avoid this, I always keep an eye on my margin levels, especially during volatile times. Staying above the maintenance requirement isn't just a suggestion—it's a necessity unless I want my broker stepping in to sell off my investments without asking. Monitoring closely helps me dodge the stress of surprise margin calls.

Consequences and Risks

When the equity in my margin account dips below the broker's maintenance requirement, I face a margin call, which forces me to act quickly or risk losing control of my investments.

A margin call isn't just a warning; it's a demand to either deposit more cash or securities or see my assets sold off to meet the requirement. This can lead to financial losses, especially if the market's already down and I'm forced to sell at a bad time.

Here's what I need to know:

- Time is limited: I usually have a short window to meet the margin call, often just a few days. Acting fast is vital to avoid losing my investments.

- Forced liquidation: If I don't comply, the broker can sell my assets without my input, sometimes at prices much lower than I'd hoped for.

- Amplified risks: Trading with borrowed money means losses can stack up quickly, especially during market volatility, making margin accounts a double-edged sword.

Managing margin accounts requires constant attention to avoid these pitfalls, but the risks are part of the game.

Interest and Fees Overview

Since I'm considering how interest and fees impact my trading costs, I'll note that margin accounts charge interest on borrowed funds, typically ranging from 5-10% annually. This can eat into returns if I'm not careful. The interest rates depend on my broker and the size of my margin balance, so borrowing more means paying more.

Transaction fees also vary, and margin accounts often have higher fees because of the added complexity of leveraging. In contrast, cash accounts don't charge interest since I'm only using my own funds, making them simpler to budget for. However, both account types may have transaction fees for trades, so I'll need to compare brokers.

Margin accounts require a minimum balance, usually $2,000, which can be a hurdle for some investors, while cash accounts don't have this requirement. If my margin balance drops below a certain level, I might also face maintenance fees, adding to the overall cost.

Watching these fees and interest charges is essential, as they can quickly add up and impact my profits, especially if I'm not actively managing my trades.

Account Management Requirements

Managing a margin account demands constant attention because I need to monitor my equity level to avoid margin calls, which can force me to liquidate assets if it falls below the broker's requirement.

Unlike Cash Accounts, where I only need to make sure I've enough cash to cover purchases, margin accounts come with more intricacies. I must maintain a minimum balance of $2,000, and my equity must stay above 25% of the total investment value to meet federal regulations. If I don't, the broker can sell my holdings without my consent—something I'd rather avoid.

Here's how I keep my margin account in check:

- Track equity daily: I stay on top of my account balance and borrowed funds to make certain I'm above the maintenance margin.

- Avoid over-leveraging: I limit how much I borrow to reduce the risk of sudden drops triggering a margin call.

- Plan for volatility: I set aside extra funds or focus on less risky trades to cushion against market swings.

With Cash Accounts, I don't face these challenges, but I also miss out on the flexibility that margin offers. It's a trade-off I weigh carefully.

Choosing the Right Account Type

How do I decide between a cash account and a margin account? First, I need to consider my risk tolerance and investment goals. Cash accounts are great if I'm a conservative investor who prefers to minimize risk and avoid borrowing. With cash accounts, I pay fully for securities upfront, so my losses are limited to the cash I've deposited. On the other hand, a margin account suits me if I'm comfortable with higher risk and want to capitalize on my investments for potentially greater returns. However, margin accounts can lead to losses exceeding my initial investment, so I'd better be prepared for that.

Here's a quick comparison to help me decide:

| Feature | Cash Account | Margin Account |

|---|---|---|

| Risk | Lower risk | Higher risk |

| Regulations | No minimum deposit typically | $2,000 minimum deposit |

| Trading Strategies | Long-term investments | Short selling, advanced strategies |

Ultimately, the choice depends on my comfort level with risk and how actively I plan to trade. If I'm unsure, I might start with a cash account and transition to a margin account later once I gain confidence and experience.

Don’t miss out on real-time market insights—sign up for TradeFT!

Leave a Reply